Deep Value Roundup

Highest conviction best ideas bucket

I’ve covered a lot of companies below net current assets and net tangible assets, in a variety of industries here over the past couple years. Today I want to go over the ones I still see as the best values.

I'm going to share the core reasons I still like the stocks and the main drivers of upside I see in each. This is part one of a two-part article. I’m going to break this one up into a couple articles as there are about a dozen or so stocks in total.

For the most part, I’m going to touch on these stocks with a broad brush. For more detailed figures click on the links to my old analysis.

Cronos Group (CRON)

I still really like Cronos Group and how well things are going for them the last year. Late last year Cronos Group (CRON) bought CanAdelaar B.V. CanAdelaar is the largest cannabis company operating in the Netherlands’ adult-use cannabis pilot program. CanAdelaar is the only industrial-scale greenhouse cultivator among the ten licensed producers in the country’s Wietexperiment program. They got a good price. The acquisition will cost $67 million in cash upfront, with additional contingent payments based on CanAdelaar’s performance in 2026 and 2027. The upfront is just aproximetely 1.4x CanAdelaar’s trailing twelve-month revenue and 2.4x its EBITDA.

Cronos’ CEO calls the CanAdelaar purchase a “highly strategic transaction that will establish a strategic presence in Europe.”

One of the important things I like about Cronos is management’s ability to execute. The company has been doing extremely well on gross margin over recent quarters. Last quarters gross margin was 51%! This is really attractive vs the competition.

I like the international growth strategy. One of the potentially big long-term growth drivers is expansion into the US market. They will do very well regardless of this materializing soon or not, however.

Some of the other big reasons I like the stock is because of the pristine balance sheet with a ton of cash and no long-term debt. The financial performance overall is a big positive. Sales are growing and they have strong market share in Canada and Israel. The big long-term growth driver is their international growth prospects.

Fourth quarter and full year earnings is coming up this Thursday the 26th of this month.

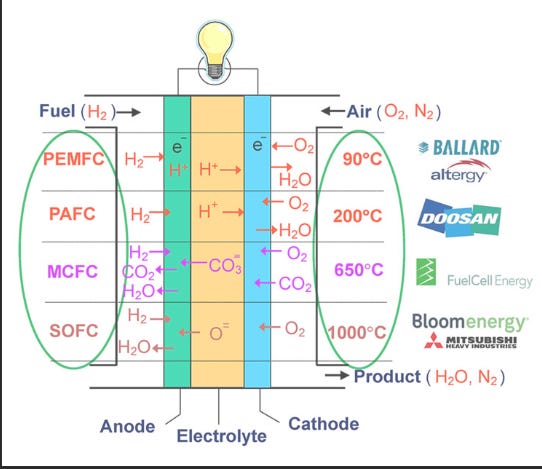

FuelCell (FCEL)

One of the main things I like with FuelCell (FCEL) is the growth potential. I’m very bullish on fuel cells. Management is in talks with hyperscalers. They benefit from the tech industry’s awareness of the potential for fuel cells after Bloom Energy’s BE surge in hyperscaler sales last year. Different energy sources outside of the traditional are much needed to meet continued data center expansion and electric grid demands.

My base case for me is FuelCell gets a significant amount of data center power backup deals at the least.

Plug Power (PLUG)

Plug Power is another fuel cell company I originally found in deep value land. Plug’s electrolyzers are their big advantage. They use electricity to split purified water into super clean hydrogen and oxygen. A company can simply build a solar farm and get that solar electricity to power an electrolyzer. You use a transformer with a rectifier and AC/DC converters to convert the PV into a stable direct current. Then the electrolyzers create green hydrogen that is used for fuel. The green hydrogen is fuel for fuel cell and turbine power, industrial processes, or be blended into gas grids.

Plug Power’s H2 Hollandia project in the Netherlands does exactly this.

Construction is underway at H2 Hollandia where Plug Power is installing a 5 MW PEM electrolyzer that is directly connected to an adjacent 115‑MWp solar park. Surplus solar electricity runs the electrolyzer to produce green hydrogen.

This solar park model could be used to fill part of the energy capacity shortfall here in the US. To get more stable power if needed they can be supplemented with batteries.

The other big thing going for them is they are in talks with three major data center operators and engaged in initial tests with all of them. Big multi-year contracts with multiple hyperscalers are not all baked into FuelCell (FCEL) and Plug Power’s (PLUG) current stock prices.

Plug is especially a contrarian trade right now. Green hydrogen is like a foreign concept to most but there are 76 green hydrogen projects planned in the US over the next few years for $36 billion in investment.

The Hydrogen Council’s Hydrogen Insights report says around 1700 clean-hydrogen projects have been announced across more than 70 countries, up from just 228 in 2020. There is atleast $110 bil in total investment so far.

Plug has been scaling up lately. The total contracted electrolyzer capacity between Plug and its newer Allied partners project is now 5 GW across two projects (3 GW in Australia + 2 GW Uzbekistan). The companies framed this as one of the largest electrolyzer supply agreements globally, moving hydrogen from MoUs to “multi‑GW, real projects.”

Plug Power worked with Microsoft in 2022 on a hydrogen fuel cell power backup proof of concept that was successful. They can provide power backup for data centers. I see data center backup power contracts being a significant catalyst for the company soon.

American Outdoor Brands (AOUT)

This Smith & Wesson spin-off has a lot of things going for it. The things I like the most about AOUT are the durable brands, strong international growth and solid management. Management has been buying back stock the past five years.

International sales in the past have grown double-digit, outpacing domestic sales. They are a very small percentage of revenue, less than 5%. I see international growth being a long-term shareholder value driver. AOUT grows revenue without heavy capex so margin-accretive international sales will grow earnings.

Being a spin-off of Smith & Wesson, they benefit from cooperation in brand licensing and some shared lease agreements.

Let’s not forgot the best thing about it. The still cheap valuation. There is $110 mil in net tangible assets vs a $118 mil market cap.

Acacia Research Corporation (ACTG)

Acacia Research (ACTG) is very shareholder focused and diversified into free cash flow generating businesses. Their Deflecto and Printronix businesses both generate free cash flow and are relatively non-cyclical. They grew revenue well in the last quarter. They also have grown revenue well annually over the years.

The main thing I like about the company is the value-oriented management. I see all their segments including the Benchmark oil and gas segment being a growth driver.

The market cap is still just 50% over NTAV of $268 mill.

Coffee Holding Co (JVA)

Coffee Holding Company has a lot of good things going for it.

They have more production capacity after the Empire Coffee acquisition.

Revenue has grown consistently over the last few years.

They are profitable on the bottom-line.

They were exposed to the tariffs and had a recent bad quarter because of that. But, I like the long-term business model and management’s ability to keep the business on course.

Gross margin can be a challenge sometimes but they navigate around it well. 2024 was the company’s third-best yearly performance in the company’s twenty-year history. They also grew sales 23% YoY last year.

JVA is now 50% below net current asset value.

Be on the lookout for the second part of this.

Full Disclosure: I am long CRON FCEL PLUG ACTG AOUT JVA