NCS Multistage Holdings (NCSM)

Oil & gas equipment & services company below net tangible assets

Business Overview

NCS Multistage, ticker symbol (NCSM), sell products and services in the oil and natural gas well construction business. They sell to E&P companies for onshore and offshore wells. They sell in North America and in select international markets, including the North Sea, the Middle East, Argentina and China. Canada is where the bulk of their revenue comes from with the U.S. bringing roughly half of that figure. Some of their U.S. customers are Exxon Mobile, Chevron and Shell.

Approximately 65% of their revenue was derived from hydraulic fracturing or “fracking” systems products and services and enhanced oil recovery systems. Approximately 15% was derived from Repeat Precision, and approximately 10% was well construction products and tracer diagnostics services. This mix has improved from 2016 when 90% of revenue was just fracking.

I will get to the fundamentals shortly. I see a couple catalysts that could bring a rotation into oil and gas stocks. The first being the new presidential administrations growth stance on domestic production. The second is what has been transpiring for some time and just ramped up again today.

President Donald Trump, on Tuesday the 21st announced investments worth up to $500 billion for infrastructure tied to AI by a new partnership formed by OpenAI, Oracle and SoftBank. Private companies are footing the bill and Softbank has pledged $100 billion.

There already has been a gap in energy production to meet the electricity demands from tech data center projections. I touched on this theme in the old post on the alternative energy stocks. Data centers consumed about 4.4% of total U.S. electricity in 2023, and are expected to consume between 6.7% and 12% of total U.S. electricity by 2028. Intel CEO Patrick Gelsinger in a video interview talked about how the high end of some of the high demand projections get pretty extreme. Nat gas power plants are the quickest to build.

Trump also sent an executive order on the 20th titled "Declaring a National Energy Emergency." The order is due to inadequate U.S. energy infrastructure and supply, exacerbated by previous policies and hostile foreign actions. The executive order mandates urgent action to increase domestic energy production, infrastructure, and reliability to secure national and economic security.

Key measures include using emergency authorities, expediting energy projects, granting fuel waivers, and leveraging Federal eminent domain and the Defense Production Act. The order emphasizes the immediate need for reliable, diversified energy to power industries and support technological innovation while protecting national security.

Fundamentals

Over the years, their operating results have been characteristic of the cyclical nature of oil and gas companies. They had an awful 2023, and it seems the trouble started in the second half of 2022 judging by earnings reactions in the stocks. From reading the management commentary, they had some operations trouble which brought some big losses on the bottom line.

They also had a lawsuit that settled in May 2023. The expenses for this were a whopping $40 million. The settlement was fully paid by the insurance carrier in January 2024. In August 2023 they also settled for $2 million on a service issue claim. They reversed this provision for that matter as it was settled and paid by the insurance company.

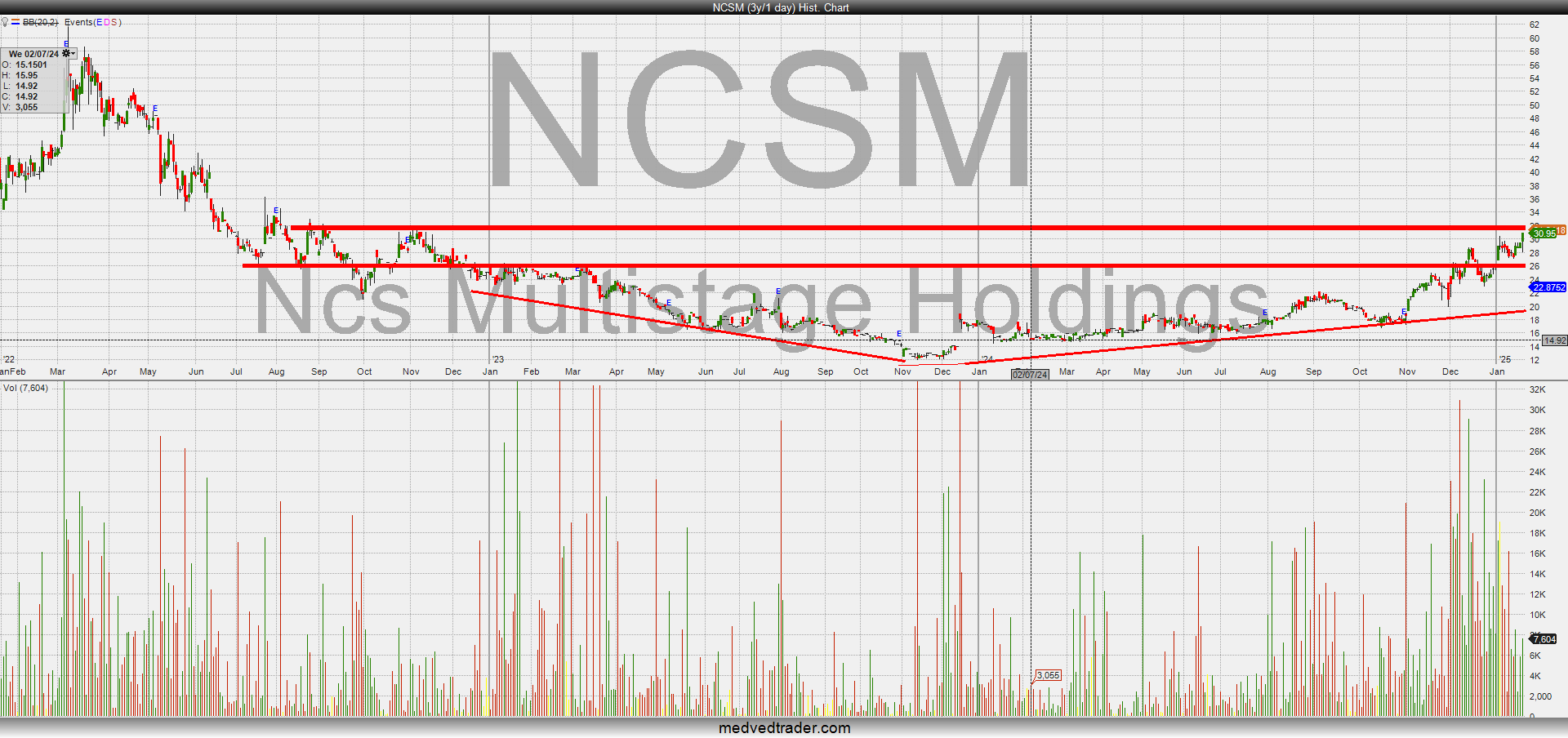

I believe all this contributed to the low sentiment that took the stock down to $12 a share in late 2023. I think many investors may have just written them off then. That gave a very good contrarian opportunity in 2024, as the stock has climbed all year.

They brought in $4.1 million in net income last quarter or $1.63 a share. In the previous quarter they had $2.5 million in net income. They still have roughly the same amount of long-term debt they've carried the last couple years at around $6.5 million.

Some other interesting things are trailing twelve month free cash flow of $6.9 million. The stock is currently trading at just 11 times TTM FCF. Return on equity TTM is 40%.

The current market cap is $77 million and net tangible asset value is $91 million. Working capital is higher than many previous years, and the balance sheet is solid with a 4.5 current ratio. They have roughly the same amount of long-term debt they've carried over recent years, at around $6.5 million. It was 6.5 mil in 2021.

Price Analysis

I paired NCSM with crude oil itself, and they tracked very closely for some time years back. That correlation failed lately until possibly this year, as crude as been flat but had some momentum from September. NCSM has had very strong momentum and relative strength the second half of this year. The stock is coming off another bull flag and is poised to break out to new monthly highs again.

Final Thoughts

I just found this one last night. Due to the industry it is in I see this one as a cigar-butt. It may trade up to a fuller valuation and that is the time to take some profits in my view.

Full Disclosure: No position at time of writing